What happens when human exceptionalism and methodological individualism, those old saws of Western philosophy and political economics, become unthinkable in the best sciences, whether natural or social? Seriously unthinkable: not available to think with. (Donna Haraway 2016)

Young people, the GFC, the Great Recession and Austerity: Lessons from our Recent Past

In a number of spaces in the last 3 years I have published accounts of the ways in which young people in various parts of the world were made to carry a particularly heavy burden for many of the downstream effects of the Global Financial Crisis (GFC) of 2008-2009.

The program of research that we are developing in the context of COVID-19 is, to a large degree, informed by the historical precedent in which young people are vulnerable in various and diverse ways, both to the more immediate social, cultural, economic and policy consequences of this public health crisis, and to the longer term ‘down-stream’ consequences of this crisis.

In this article I argued that in the aftermath of the Global Financial Crisis of 2008–2009 young people, certain populations of young people in particular, were made to bear a heavy burden, carry significant responsibilities for re-imagining their lives as a enterprise – an enterprise in which an investment in education and training and work increasingly looked like a mortgaging of an uncertain future. Elements of the argument are sketched below:

…The GFC and generations

In many of the Organisation for Economic Co-operation and Development (OECD) economies, young people appear to be carrying a particularly heavy burden for many of the downstream effects of the 2008–2009 GFC. These downstream effects have compounded the educational and labour market effects and consequences of 30 or 40 years of heightened globalisation, the emergence of a more flexible capitalism, and the ways in which 1980s Thatcherism and Reaganism have morphed into the globalised triumphalism of neo-Liberalism (Hall, Massey, & Rustin, 2013).

The unfolding effects of what some are calling the Great Recession in Europe and the USA, and the emergence of sovereign debt crises and significant austerity programs in many European Union (EU)/OECD economies represent a largely successful framing of responses to the downstream effects of the GFC as being principally about State debt levels. In this discourse those that depend most on State provided services, payments and programmes will be the ones to carry the greatest burden of government austerity measures. In an appearance before the UK’s House of Commons Treasury Committee in early 2011, the then Governor of the Bank of England Mervyn King claimed that those made unemployed or who had their benefits cut as a consequence of the GFC, recession and austerity ‘had every reason to be resentful and voice their protest’. In his submission to the Committee he suggested: that the billions spent bailing out the banks and the need for public spending cuts were the fault of the financial services sector: ‘The price of this financial crisis is being borne by people who absolutely did not cause it’. (cited in Inman, 2011)…’

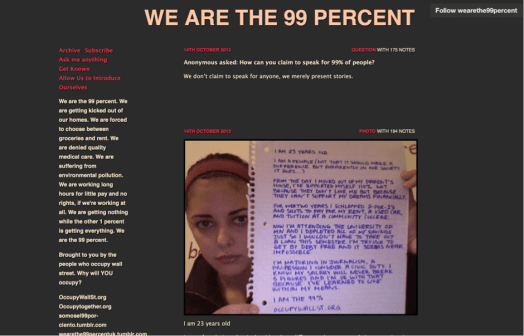

‘…These concerns are well captured by the many hundreds, even thousands of contributions from young people to a Tumblr page called We Are the 99%. Those who posted to this page were asked to upload an image, and to contribute some text about the image and why they imagined themselves as being part of the 99%. I want to present just a small number of these posts. In the first one a forlorn looking young woman, wearing headphones and looking into her computer’s camera, holds up a notebook where she has written:

I CAN’T FIND MY FUTURE.

I looked in college.

I found debt.

I looked to my parents.

I found debt and heartbreak.

I looked at my friends.

I found grief and sorrow.

I looked at the land.

I found MY COMMONS DESTROYED, MY LAKES AND RIVERS AND SOIL

AND TREES AND BEES AND WORMS DESTROYED.

I looked at my fellow humans.

I found disease, debt, sorrow, dissonance, hate, greed, misery,

AND NO ONE CARES ANYMORE.

well. I CARE. an awful lot.

I’M TAKING MY FUTURE BACK.

(IT’S MINE)

I AM THE 99%…

‘…In the aftermath of the GFC, as a consequence of largely successful neo-Liberal attempts to re-configure this aftermath as being principally about sovereign debt crises, the need for austerity, and an end to the ‘age of entitlement’, we may be condemning generations of young people to a life-long burden of precariousness and debt. In this sense, a self as enterprise that grows up after the GFC is being made responsible for resolving the contradictions, the paradoxes, the limits and possibilities of fashioning a life in twenty-first century capitalism. That is a burden of responsibility beyond the capacities of many us, and a burden that is that much harder to bear when you have mortgaged your future on the promise that education and training will secure an always parlous salvation in the globalised and precarious labour markets of twenty-first-century capitalism…’

With my colleague Jo Pike, I co-edited a collection titled:

That collection examined the relationships between a globalising neoliberal capitalism, a post-GFC environment of recession and austerity, and the moral economies of young people’s health and well-being. Our contributors explored how in the second decade of the 21st century, many young people in the OECD/EU economies and in the developing economies of Asia, Africa and Central and South America were made to carry a particularly heavy burden for many of the downstream effects of the 2008-09 Global Financial Crisis. Our colleagues explored the ways in which increasing local and global inequalities often have profound consequences for large populations of young people. These consequences are not just related to marginalisation from education, training and work. They also included obstacles to their active participation in the civic life of their communities, to their transitions, to their sense of belonging. The edited collection examines the choices that are made, or not made by governments, businesses and individuals in relation to young people’s education, training, work, health and well-being, sexualities, diets and bodies, in the context of a crisis of neoliberalism and of austerity.

The article, the edited collection, and the other youth research that addresses similar concerns, have many lessons for how we approach our thinking about the challenges that lie ahead for populations of young people in many parts of the world as a consequence of the COVID-19 pandemic.

International Forecasts for Economic Activity and Labour Markets ‘after’ COVID-19

At this time there is a ‘flood’ of data, preliminary analyses, reports, forecasts and modelling about the economic consequences of a prolonged pandemic, and the social, cultural and policy challenges that emerge in this context. In this post we start the task of curating elements of this flow of information, with a particular focus on economic forecasts from peak agencies and think tanks with a focus on young people.

The International Monetary Fund (IMF)

The following text comes from the IMF Managing Director, Kristalina Georgieva’s Statement to a meeting of the IMF Development Committee in April 2020. Click here for access to a pdf of the full statement.

The statement, while it targets the challenges for Emerging and Developing Economies (EMDEs), points to the global dimensions of the health, social, economic and policy challenges of COVID-19.

Of interest, particularly for those commentators and policy makers who are hopeful of a quick ‘snap back’ – even a ‘V-shaped’ recession – once the public health dimensions of the crisis start to ease is that the pandemic emerged at a time of existing global economic weakness:

The coronavirus pandemic struck the global economy in an already fragile state, weighed down by trade disputes, policy uncertainty, and geopolitical tensions—even though some signs of recovery had emerged at end-2019.

Prospects have deteriorated sharply with the spread of the COVID-19 pandemic. Countries that were affected early—such as China, South Korea, and Italy—have suffered large contractions in manufacturing activity and services, exceeding the losses recorded at the onset of the global financial crisis. Retrenchments in activity have been accompanied by a sharp repricing of financial assets amid rapidly deteriorating risk sentiment, large equity sell-offs, widening risk spreads, and reversals of portfolio flows to EMDEs. Many commodity prices have fallen sharply, notably for oil.

What this suggests is that metaphors such as ‘snap-back’, ‘bounce-back’, ‘V-shaped recession’, a return to ‘business-as-usual’ might prove to be overly optimistic, even premature:

A large global contraction in the first half of 2020 is inevitable. Prospects thereafter depend on the intensity and efficacy of containment efforts, progress with developing vaccines and therapies, the extent of supply disruptions, shifts in spending patterns, the impact of tighter financial conditions on activity, and the size of the policy response.

Assuming the global economy starts recovering from the third quarter—as public health measures are scaled back and the impact of policy support materializes—the level of global GDP in 2020 would still decline substantially relative to 2019, with a contraction significantly worse than that in 2009 in the context of the global financial crisis (and compared to real growth of 2.9 percent in 2019). While the recovery is expected to pick up in 2021, by end-2021 global output would remain significantly below the pre-crisis trend.

In much of this commentary – including here by the IMF – there are attempts to make comparisons with the levels of economic downturn after the GFC, often with a sense that this time is different to the GFC. At the same time there is little, if any acknowledgement that the decade long recession in many OECD contexts that was associated with government austerity measures that followed the immediate ‘stimulus’ to global financial systems, and/or of the long periods of central bank ‘Quantitative Easing’ (QE) that transferred trillions of dollars to asset holders at the expense of wage and salary earners and recipients of income/welfare support.

An alternative scenario also emerges in the early phases of this sense-making about what follows the ‘Great Shutdown’ – this might be called a ‘worst-case scenario’ and is far less optimistic for world economic activity in the immediate and more medium term:

Downside risks to the baseline scenario are large. The recovery could be slower and/or weaker than expected, for example because uncertainty about contagion lingers, and the measures to contain the spread of the virus trigger more lasting supply-chain disruptions and weaknesses in aggregate demand. A more persistent slump in business confidence could weaken investment by more than is currently projected, thus exerting a negative impact on trend growth. A protracted risk-off episode in financial markets would expose vulnerable corporate and sovereign borrowers to rollover risk, laying bare balance sheet fragilities that built up during the long phase of low global interest rates. Policy space to respond to the crisis is less than it was a decade ago, since in many countries monetary policy rates are already low and public debt is elevated.

There are series of links here to other international agencies and the resources that they producing up until the end of April 2020, while much of the world is still in shutdown.

We will return to some of these resources in coming months as the scenarios and modelling develop, and the prospects for young people in a COVID-19 world become more apparent.

Forecasts for Economic Activity and Labour Markets in Australia

More than a quarter of a million jobs could be lost in Victoria due to the coronavirus pandemic, according to “catastrophic” modelling from the Department of Treasury and Finance. Treasury forecasts 270,000 Victorians could be out of work as a result of the economic and health crisis, with Victoria’s unemployment rate peaking as high as 11 per cent in the September quarter, more than double the current rate. Victoria’s gross state product may also fall by an unprecedented 14 per cent relative to previous forecasts. The property market, a major source of government revenue, will also be hit, with prices predicted to fall by up to 9 per cent by the end of the year. “These figures are bleak, they’re quite frankly quite catastrophic,” Treasurer Tim Pallas said, adding it would take years for the Victorian economy to fully recover.

At the end of April 2020, there is an emerging picture that is pointing to the severe economic, social, cultural and policy consequences of the pandemic in Australia, and for particular parts of Australia, and for particular populations of Australians. At the same time this ‘picture’ is still uncertain, and the different scenarios – from ‘best case’ to ‘worst case’ – point to very different outcomes for different parts of the economy and for different places, communities and populations.

We will revisit these scenarios in the coming months and beyond.

In this post we just want to briefly discuss a report by the Grattan Institute. [1]

The report, Shutdown: estimating the COVID-19 employment shock, offers a very preliminary analysis of the immediate labour market impacts of the shutdown due to the pandemic. This analysis is framed by three different methodologies – a preferred method, and two alternatives – that produce very different outcomes.[2] As the report indicates:

The economic situation facing Australia and other advanced economies is quite literally unprecedented. The pandemic-induced shutdown does not resemble ‘ordinary’ recessions, and previous pandemics have not been of the same magnitude, or they occurred so long ago that few relevant economic insights can be gleaned from them. This means that estimating the size of the COVID-19 employment shock is particularly difficult. This working paper represents our best attempt to forecast the size of the shock, under conditions of extreme uncertainty and limited information. (p.14)

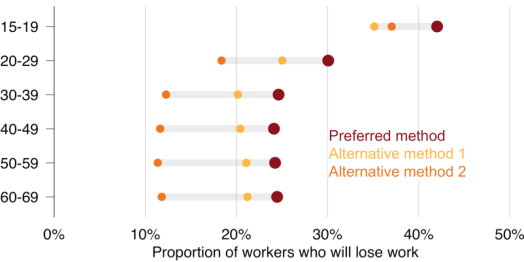

Our interest at this time is with the following section (p.22) that forecasts that younger workers (those aged 15-29), and women, will likely be most heavily impacted in terms of job losses.

3.3 Younger workers and women will be hit hardest – but plenty of older workers and men will lose their jobs, too.

Given that the hospitality industry is expected to suffer the biggest loss of jobs (Figure 3.2), it is perhaps unsurprising that young people will be hardest hit.

We estimate that about 40 per cent of employed teenagers will lose work due to the COVID-19 shutdown and spatial distancing. People in their 20s are the next most-likely to lose work. All other age groups have a broadly-similar prospect of losing work, as shown in Figure 3.4.

The proportion of workers who will be thrown out of work by the COVID-19 response is high for all age groups – around a quarter of workers even in the older age groups.

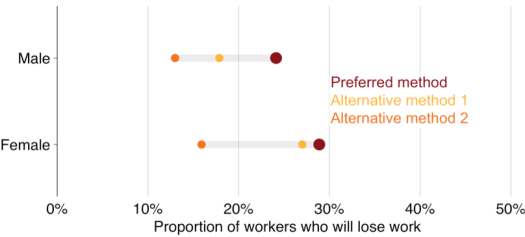

Women are disproportionately likely to be employed in the occupations and industries most affected by the response to COVID-19. We find that they face a higher probability of losing their jobs than men (see Figure 3.4).

Figure 3.4a: Estimated percentage of workers who will be out of work, by age:

Coates, B., Cowgill, M., Chen, T., and Mackey, W. (2020). Shutdown: estimating the COVID-19 employment shock. Grattan Institute. Click here for a pdf version of the report.

Figure 3.4b: Estimated percentage of workers who will lose their jobs, by gender

Coates, B., Cowgill, M., Chen, T., and Mackey, W. (2020). Shutdown: estimating the COVID-19 employment shock. Grattan Institute. Click here for a pdf version of the report.

The immediate health, social, economic and policy dimensions of COVID-19 are devastating. Many claim that, ‘we-are-all-in-this-together’. But, as Rosi Braidotti has argued, ‘we-may-all-be-in-this-together-but-we-are-not-all-the-same’.

Our research program acknowledges this, and seeks to work with others to develop scenarios that are informed by, and address the temporal, spatial, and demographic forces and processes that are entangled with the COVID-19 pandemic, with processes of digital disruption and globalisation, and with the histories of the past 30 years which have produced widening health, education and employment inequalities – particularly for different populations of young people in different places.

[1] The Grattan Institute is an Australian public policy think tank, established in 2008. The Melbourne-based institute is non-aligned, however it defines itself as contributing “to public policy in Australia as a liberal democracy in a globalised economy.” https://en.wikipedia.org/wiki/Grattan_Institute

[2] These methodologies are described and discussed in detail in chapter 2 of the report, on pp. 14-19.

‘…These concerns are well captured by the many hundreds, even thousands of contributions from young people to a Tumblr page called We Are the 99%. Those who posted to this page were asked to upload an image, and to contribute some text about the image and why they imagined themselves as being part of the 99%. I want to present just a small number of these posts. In the first one a forlorn looking young woman, wearing headphones and looking into her computer’s camera, holds up a notebook where she has written:

‘…These concerns are well captured by the many hundreds, even thousands of contributions from young people to a Tumblr page called We Are the 99%. Those who posted to this page were asked to upload an image, and to contribute some text about the image and why they imagined themselves as being part of the 99%. I want to present just a small number of these posts. In the first one a forlorn looking young woman, wearing headphones and looking into her computer’s camera, holds up a notebook where she has written: With my colleague Jo Pike, I co-edited a collection titled:

With my colleague Jo Pike, I co-edited a collection titled:

What this suggests is that metaphors such as ‘snap-back’, ‘bounce-back’, ‘V-shaped recession’, a return to ‘business-as-usual’ might prove to be overly optimistic, even premature:

What this suggests is that metaphors such as ‘snap-back’, ‘bounce-back’, ‘V-shaped recession’, a return to ‘business-as-usual’ might prove to be overly optimistic, even premature:

One Reply to “”